Tidy summarizes information about the components of a model. A model component might be a single term in a regression, a single hypothesis, a cluster, or a class. Exactly what tidy considers to be a model component varies across models but is usually self-evident. If a model has several distinct types of components, you will need to specify which components to return.

Usage

# S3 method for class 'gmm'

tidy(x, conf.int = FALSE, conf.level = 0.95, exponentiate = FALSE, ...)Arguments

- x

A

gmmobject returned fromgmm::gmm().- conf.int

Logical indicating whether or not to include a confidence interval in the tidied output. Defaults to

FALSE.- conf.level

The confidence level to use for the confidence interval if

conf.int = TRUE. Must be strictly greater than 0 and less than 1. Defaults to 0.95, which corresponds to a 95 percent confidence interval.- exponentiate

Logical indicating whether or not to exponentiate the the coefficient estimates. This is typical for logistic and multinomial regressions, but a bad idea if there is no log or logit link. Defaults to

FALSE.- ...

Additional arguments. Not used. Needed to match generic signature only. Cautionary note: Misspelled arguments will be absorbed in

..., where they will be ignored. If the misspelled argument has a default value, the default value will be used. For example, if you passconf.lvel = 0.9, all computation will proceed usingconf.level = 0.95. Two exceptions here are:

See also

Other gmm tidiers:

glance.gmm()

Value

A tibble::tibble() with columns:

- conf.high

Upper bound on the confidence interval for the estimate.

- conf.low

Lower bound on the confidence interval for the estimate.

- estimate

The estimated value of the regression term.

- p.value

The two-sided p-value associated with the observed statistic.

- statistic

The value of a T-statistic to use in a hypothesis that the regression term is non-zero.

- std.error

The standard error of the regression term.

- term

The name of the regression term.

Examples

# load libraries for models and data

library(gmm)

# examples come from the "gmm" package

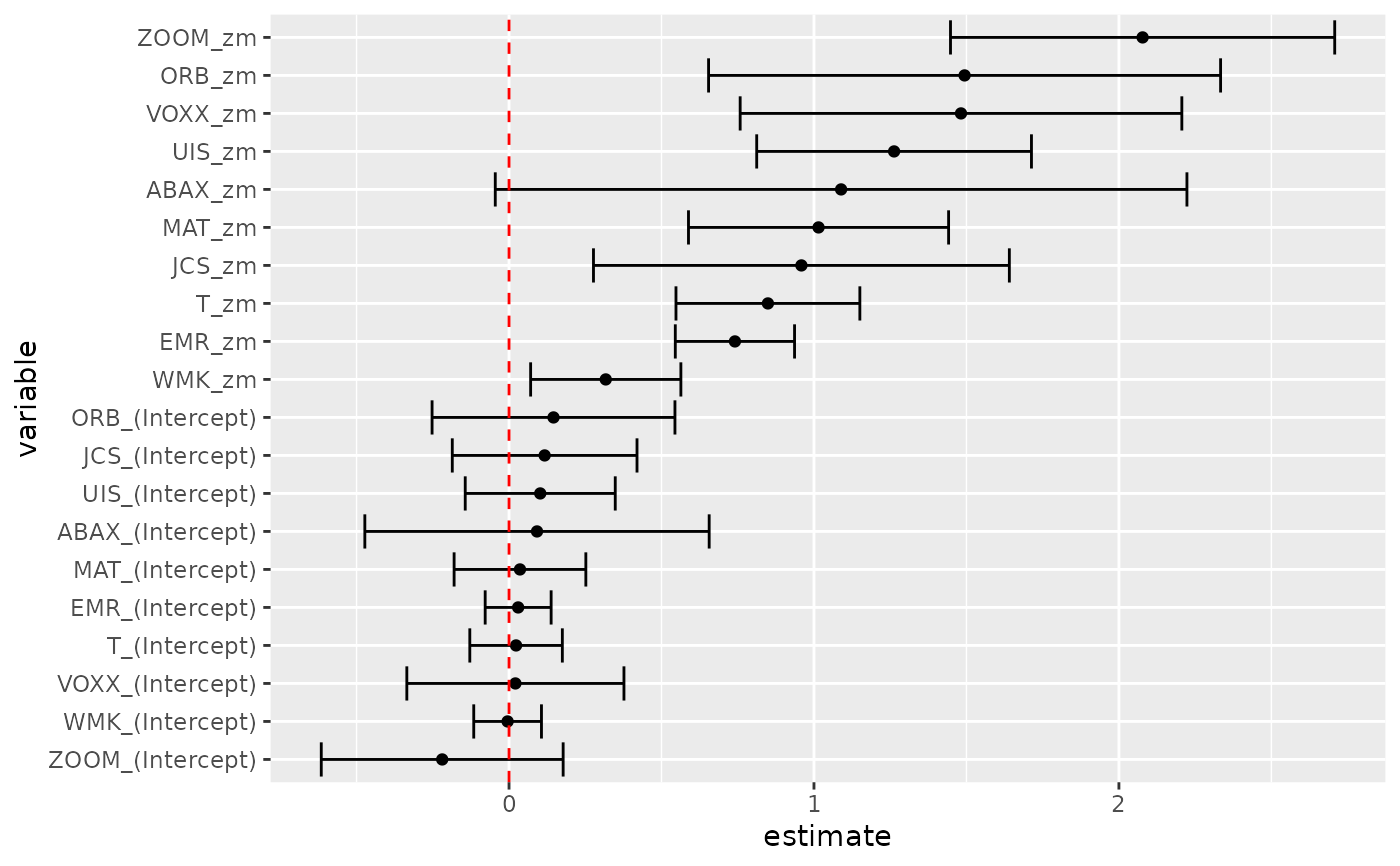

# CAPM test with GMM

data(Finance)

r <- Finance[1:300, 1:10]

rm <- Finance[1:300, "rm"]

rf <- Finance[1:300, "rf"]

z <- as.matrix(r - rf)

t <- nrow(z)

zm <- rm - rf

h <- matrix(zm, t, 1)

res <- gmm(z ~ zm, x = h)

# tidy result

tidy(res)

#> # A tibble: 20 × 5

#> term estimate std.error statistic p.value

#> <chr> <dbl> <dbl> <dbl> <dbl>

#> 1 WMK_(Intercept) -0.00467 0.0566 -0.0824 9.34e- 1

#> 2 UIS_(Intercept) 0.102 0.126 0.816 4.15e- 1

#> 3 ORB_(Intercept) 0.146 0.203 0.718 4.73e- 1

#> 4 MAT_(Intercept) 0.0359 0.110 0.326 7.45e- 1

#> 5 ABAX_(Intercept) 0.0917 0.288 0.318 7.50e- 1

#> 6 T_(Intercept) 0.0231 0.0774 0.298 7.65e- 1

#> 7 EMR_(Intercept) 0.0299 0.0552 0.542 5.88e- 1

#> 8 JCS_(Intercept) 0.117 0.155 0.756 4.50e- 1

#> 9 VOXX_(Intercept) 0.0209 0.182 0.115 9.09e- 1

#> 10 ZOOM_(Intercept) -0.219 0.202 -1.08 2.79e- 1

#> 11 WMK_zm 0.317 0.126 2.52 1.16e- 2

#> 12 UIS_zm 1.26 0.230 5.49 3.94e- 8

#> 13 ORB_zm 1.49 0.428 3.49 4.87e- 4

#> 14 MAT_zm 1.01 0.218 4.66 3.09e- 6

#> 15 ABAX_zm 1.09 0.579 1.88 5.98e- 2

#> 16 T_zm 0.849 0.154 5.52 3.41e- 8

#> 17 EMR_zm 0.741 0.0998 7.43 1.13e-13

#> 18 JCS_zm 0.959 0.348 2.76 5.85e- 3

#> 19 VOXX_zm 1.48 0.369 4.01 6.04e- 5

#> 20 ZOOM_zm 2.08 0.321 6.46 1.02e-10

tidy(res, conf.int = TRUE)

#> # A tibble: 20 × 7

#> term estimate std.error statistic p.value conf.low conf.high

#> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 WMK_(Inter… -0.00467 0.0566 -0.0824 9.34e- 1 -0.116 0.106

#> 2 UIS_(Inter… 0.102 0.126 0.816 4.15e- 1 -0.144 0.348

#> 3 ORB_(Inter… 0.146 0.203 0.718 4.73e- 1 -0.252 0.544

#> 4 MAT_(Inter… 0.0359 0.110 0.326 7.45e- 1 -0.180 0.252

#> 5 ABAX_(Inte… 0.0917 0.288 0.318 7.50e- 1 -0.473 0.656

#> 6 T_(Interce… 0.0231 0.0774 0.298 7.65e- 1 -0.129 0.175

#> 7 EMR_(Inter… 0.0299 0.0552 0.542 5.88e- 1 -0.0782 0.138

#> 8 JCS_(Inter… 0.117 0.155 0.756 4.50e- 1 -0.186 0.420

#> 9 VOXX_(Inte… 0.0209 0.182 0.115 9.09e- 1 -0.335 0.377

#> 10 ZOOM_(Inte… -0.219 0.202 -1.08 2.79e- 1 -0.616 0.177

#> 11 WMK_zm 0.317 0.126 2.52 1.16e- 2 0.0708 0.564

#> 12 UIS_zm 1.26 0.230 5.49 3.94e- 8 0.812 1.71

#> 13 ORB_zm 1.49 0.428 3.49 4.87e- 4 0.654 2.33

#> 14 MAT_zm 1.01 0.218 4.66 3.09e- 6 0.588 1.44

#> 15 ABAX_zm 1.09 0.579 1.88 5.98e- 2 -0.0451 2.22

#> 16 T_zm 0.849 0.154 5.52 3.41e- 8 0.547 1.15

#> 17 EMR_zm 0.741 0.0998 7.43 1.13e-13 0.545 0.936

#> 18 JCS_zm 0.959 0.348 2.76 5.85e- 3 0.277 1.64

#> 19 VOXX_zm 1.48 0.369 4.01 6.04e- 5 0.758 2.21

#> 20 ZOOM_zm 2.08 0.321 6.46 1.02e-10 1.45 2.71

tidy(res, conf.int = TRUE, conf.level = .99)

#> # A tibble: 20 × 7

#> term estimate std.error statistic p.value conf.low conf.high

#> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 WMK_(Inter… -0.00467 0.0566 -0.0824 9.34e- 1 -0.151 0.141

#> 2 UIS_(Inter… 0.102 0.126 0.816 4.15e- 1 -0.221 0.426

#> 3 ORB_(Inter… 0.146 0.203 0.718 4.73e- 1 -0.377 0.669

#> 4 MAT_(Inter… 0.0359 0.110 0.326 7.45e- 1 -0.248 0.320

#> 5 ABAX_(Inte… 0.0917 0.288 0.318 7.50e- 1 -0.650 0.834

#> 6 T_(Interce… 0.0231 0.0774 0.298 7.65e- 1 -0.176 0.223

#> 7 EMR_(Inter… 0.0299 0.0552 0.542 5.88e- 1 -0.112 0.172

#> 8 JCS_(Inter… 0.117 0.155 0.756 4.50e- 1 -0.281 0.515

#> 9 VOXX_(Inte… 0.0209 0.182 0.115 9.09e- 1 -0.447 0.489

#> 10 ZOOM_(Inte… -0.219 0.202 -1.08 2.79e- 1 -0.740 0.302

#> 11 WMK_zm 0.317 0.126 2.52 1.16e- 2 -0.00656 0.641

#> 12 UIS_zm 1.26 0.230 5.49 3.94e- 8 0.671 1.85

#> 13 ORB_zm 1.49 0.428 3.49 4.87e- 4 0.391 2.60

#> 14 MAT_zm 1.01 0.218 4.66 3.09e- 6 0.454 1.58

#> 15 ABAX_zm 1.09 0.579 1.88 5.98e- 2 -0.401 2.58

#> 16 T_zm 0.849 0.154 5.52 3.41e- 8 0.453 1.25

#> 17 EMR_zm 0.741 0.0998 7.43 1.13e-13 0.484 0.998

#> 18 JCS_zm 0.959 0.348 2.76 5.85e- 3 0.0627 1.85

#> 19 VOXX_zm 1.48 0.369 4.01 6.04e- 5 0.530 2.43

#> 20 ZOOM_zm 2.08 0.321 6.46 1.02e-10 1.25 2.91

# coefficient plot

library(ggplot2)

library(dplyr)

tidy(res, conf.int = TRUE) |>

mutate(variable = reorder(term, estimate)) |>

ggplot(aes(estimate, variable)) +

geom_point() +

geom_errorbarh(aes(xmin = conf.low, xmax = conf.high)) +

geom_vline(xintercept = 0, color = "red", lty = 2)

# from a function instead of a matrix

g <- function(theta, x) {

e <- x[, 2:11] - theta[1] - (x[, 1] - theta[1]) %*% matrix(theta[2:11], 1, 10)

gmat <- cbind(e, e * c(x[, 1]))

return(gmat)

}

x <- as.matrix(cbind(rm, r))

res_black <- gmm(g, x = x, t0 = rep(0, 11))

tidy(res_black)

#> # A tibble: 11 × 5

#> term estimate std.error statistic p.value

#> <chr> <dbl> <dbl> <dbl> <dbl>

#> 1 Theta[1] 0.516 0.172 3.00 2.72e- 3

#> 2 Theta[2] 1.12 0.116 9.65 5.02e-22

#> 3 Theta[3] 0.680 0.197 3.45 5.65e- 4

#> 4 Theta[4] -0.0322 0.424 -0.0761 9.39e- 1

#> 5 Theta[5] 0.850 0.155 5.49 4.05e- 8

#> 6 Theta[6] -0.205 0.479 -0.429 6.68e- 1

#> 7 Theta[7] 0.625 0.122 5.14 2.73e- 7

#> 8 Theta[8] 1.05 0.0687 15.3 5.03e-53

#> 9 Theta[9] 0.640 0.233 2.75 5.92e- 3

#> 10 Theta[10] 0.596 0.295 2.02 4.36e- 2

#> 11 Theta[11] 1.16 0.240 4.82 1.45e- 6

tidy(res_black, conf.int = TRUE)

#> # A tibble: 11 × 7

#> term estimate std.error statistic p.value conf.low conf.high

#> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 Theta[1] 0.516 0.172 3.00 2.72e- 3 0.178 0.853

#> 2 Theta[2] 1.12 0.116 9.65 5.02e-22 0.889 1.34

#> 3 Theta[3] 0.680 0.197 3.45 5.65e- 4 0.293 1.07

#> 4 Theta[4] -0.0322 0.424 -0.0761 9.39e- 1 -0.862 0.798

#> 5 Theta[5] 0.850 0.155 5.49 4.05e- 8 0.546 1.15

#> 6 Theta[6] -0.205 0.479 -0.429 6.68e- 1 -1.14 0.733

#> 7 Theta[7] 0.625 0.122 5.14 2.73e- 7 0.387 0.864

#> 8 Theta[8] 1.05 0.0687 15.3 5.03e-53 0.919 1.19

#> 9 Theta[9] 0.640 0.233 2.75 5.92e- 3 0.184 1.10

#> 10 Theta[10] 0.596 0.295 2.02 4.36e- 2 0.0171 1.17

#> 11 Theta[11] 1.16 0.240 4.82 1.45e- 6 0.686 1.63

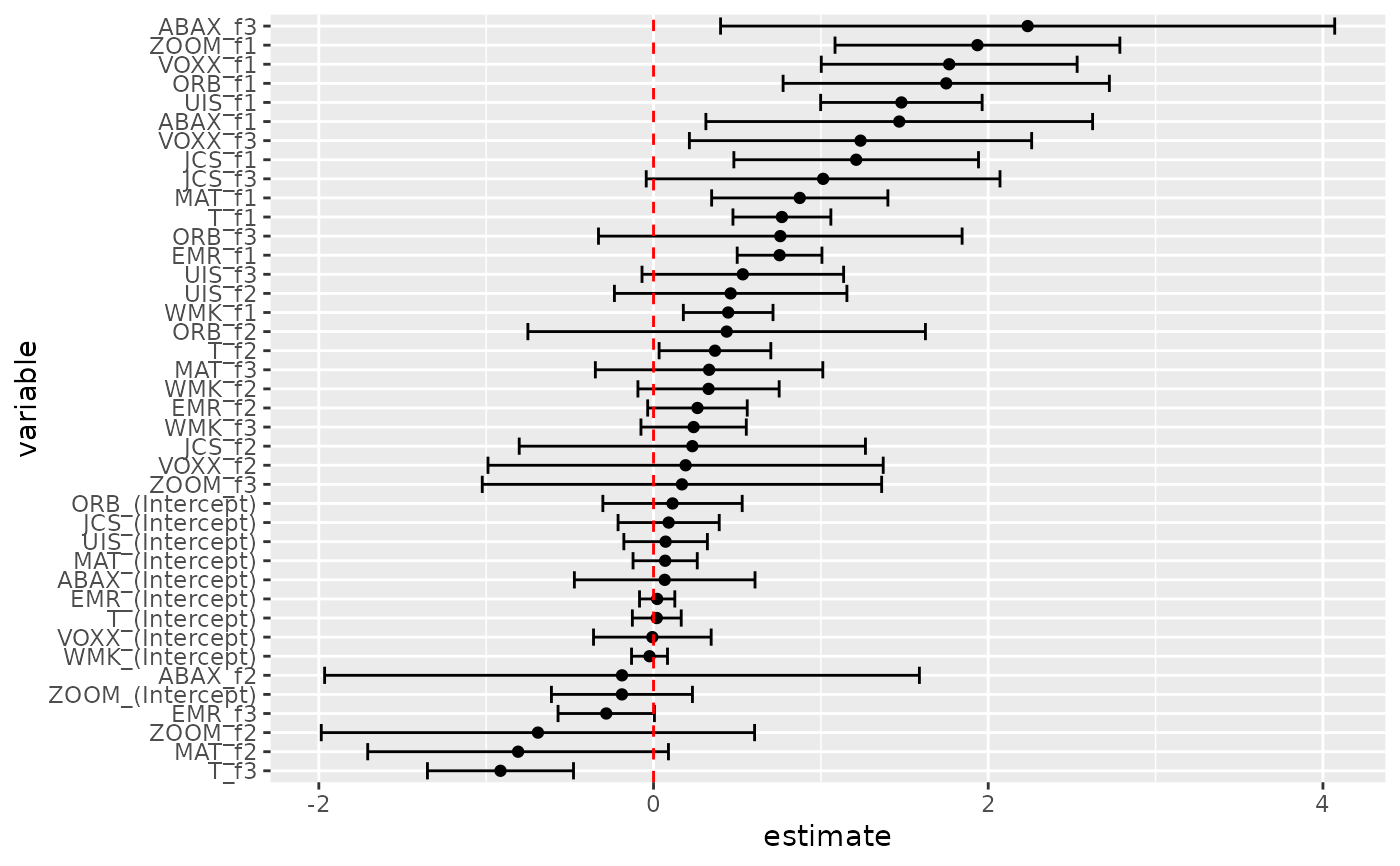

# APT test with Fama-French factors and GMM

f1 <- zm

f2 <- Finance[1:300, "hml"] - rf

f3 <- Finance[1:300, "smb"] - rf

h <- cbind(f1, f2, f3)

res2 <- gmm(z ~ f1 + f2 + f3, x = h)

td2 <- tidy(res2, conf.int = TRUE)

td2

#> # A tibble: 40 × 7

#> term estimate std.error statistic p.value conf.low conf.high

#> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 WMK_(Interc… -0.0240 0.0548 -0.438 0.662 -0.131 0.0834

#> 2 UIS_(Interc… 0.0723 0.127 0.567 0.570 -0.177 0.322

#> 3 ORB_(Interc… 0.114 0.212 0.534 0.593 -0.303 0.530

#> 4 MAT_(Interc… 0.0694 0.0979 0.709 0.478 -0.122 0.261

#> 5 ABAX_(Inter… 0.0668 0.275 0.242 0.808 -0.473 0.606

#> 6 T_(Intercep… 0.0195 0.0745 0.262 0.793 -0.126 0.165

#> 7 EMR_(Interc… 0.0217 0.0538 0.404 0.687 -0.0837 0.127

#> 8 JCS_(Interc… 0.0904 0.154 0.586 0.558 -0.212 0.393

#> 9 VOXX_(Inter… -0.00706 0.179 -0.0394 0.969 -0.359 0.344

#> 10 ZOOM_(Inter… -0.189 0.215 -0.878 0.380 -0.610 0.233

#> # ℹ 30 more rows

# coefficient plot

td2 |>

mutate(variable = reorder(term, estimate)) |>

ggplot(aes(estimate, variable)) +

geom_point() +

geom_errorbarh(aes(xmin = conf.low, xmax = conf.high)) +

geom_vline(xintercept = 0, color = "red", lty = 2)

# from a function instead of a matrix

g <- function(theta, x) {

e <- x[, 2:11] - theta[1] - (x[, 1] - theta[1]) %*% matrix(theta[2:11], 1, 10)

gmat <- cbind(e, e * c(x[, 1]))

return(gmat)

}

x <- as.matrix(cbind(rm, r))

res_black <- gmm(g, x = x, t0 = rep(0, 11))

tidy(res_black)

#> # A tibble: 11 × 5

#> term estimate std.error statistic p.value

#> <chr> <dbl> <dbl> <dbl> <dbl>

#> 1 Theta[1] 0.516 0.172 3.00 2.72e- 3

#> 2 Theta[2] 1.12 0.116 9.65 5.02e-22

#> 3 Theta[3] 0.680 0.197 3.45 5.65e- 4

#> 4 Theta[4] -0.0322 0.424 -0.0761 9.39e- 1

#> 5 Theta[5] 0.850 0.155 5.49 4.05e- 8

#> 6 Theta[6] -0.205 0.479 -0.429 6.68e- 1

#> 7 Theta[7] 0.625 0.122 5.14 2.73e- 7

#> 8 Theta[8] 1.05 0.0687 15.3 5.03e-53

#> 9 Theta[9] 0.640 0.233 2.75 5.92e- 3

#> 10 Theta[10] 0.596 0.295 2.02 4.36e- 2

#> 11 Theta[11] 1.16 0.240 4.82 1.45e- 6

tidy(res_black, conf.int = TRUE)

#> # A tibble: 11 × 7

#> term estimate std.error statistic p.value conf.low conf.high

#> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 Theta[1] 0.516 0.172 3.00 2.72e- 3 0.178 0.853

#> 2 Theta[2] 1.12 0.116 9.65 5.02e-22 0.889 1.34

#> 3 Theta[3] 0.680 0.197 3.45 5.65e- 4 0.293 1.07

#> 4 Theta[4] -0.0322 0.424 -0.0761 9.39e- 1 -0.862 0.798

#> 5 Theta[5] 0.850 0.155 5.49 4.05e- 8 0.546 1.15

#> 6 Theta[6] -0.205 0.479 -0.429 6.68e- 1 -1.14 0.733

#> 7 Theta[7] 0.625 0.122 5.14 2.73e- 7 0.387 0.864

#> 8 Theta[8] 1.05 0.0687 15.3 5.03e-53 0.919 1.19

#> 9 Theta[9] 0.640 0.233 2.75 5.92e- 3 0.184 1.10

#> 10 Theta[10] 0.596 0.295 2.02 4.36e- 2 0.0171 1.17

#> 11 Theta[11] 1.16 0.240 4.82 1.45e- 6 0.686 1.63

# APT test with Fama-French factors and GMM

f1 <- zm

f2 <- Finance[1:300, "hml"] - rf

f3 <- Finance[1:300, "smb"] - rf

h <- cbind(f1, f2, f3)

res2 <- gmm(z ~ f1 + f2 + f3, x = h)

td2 <- tidy(res2, conf.int = TRUE)

td2

#> # A tibble: 40 × 7

#> term estimate std.error statistic p.value conf.low conf.high

#> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 WMK_(Interc… -0.0240 0.0548 -0.438 0.662 -0.131 0.0834

#> 2 UIS_(Interc… 0.0723 0.127 0.567 0.570 -0.177 0.322

#> 3 ORB_(Interc… 0.114 0.212 0.534 0.593 -0.303 0.530

#> 4 MAT_(Interc… 0.0694 0.0979 0.709 0.478 -0.122 0.261

#> 5 ABAX_(Inter… 0.0668 0.275 0.242 0.808 -0.473 0.606

#> 6 T_(Intercep… 0.0195 0.0745 0.262 0.793 -0.126 0.165

#> 7 EMR_(Interc… 0.0217 0.0538 0.404 0.687 -0.0837 0.127

#> 8 JCS_(Interc… 0.0904 0.154 0.586 0.558 -0.212 0.393

#> 9 VOXX_(Inter… -0.00706 0.179 -0.0394 0.969 -0.359 0.344

#> 10 ZOOM_(Inter… -0.189 0.215 -0.878 0.380 -0.610 0.233

#> # ℹ 30 more rows

# coefficient plot

td2 |>

mutate(variable = reorder(term, estimate)) |>

ggplot(aes(estimate, variable)) +

geom_point() +

geom_errorbarh(aes(xmin = conf.low, xmax = conf.high)) +

geom_vline(xintercept = 0, color = "red", lty = 2)